2016 – a messy but okay year

US share market analyst Joe Granville once observed that “if it’s obvious, it’s obviously wrong”. 2016 was perhaps remarkable for the things that many thought were obvious at the start of the year but did not happen: the global economy did not see plunging growth and deflation; the Fed did not blindly raise interest rates; commodity prices did not continue to crash; the Brexit vote did not plunge the world into a growth slump; the election of Donald Trump did not cause a share market crash; China did not hard land (again); Europe did not break apart; tensions in the South China Sea did not bubble over into war; and the Australian property market did not collapse. What did happen was far more mundane:

-

The global economy continued to muddle along, at around 3% growth. The good news is that growth indicators stabilised and improved through the year helped in particular by stronger growth in the US after a slow start and a stabilisation in Chinese growth.

-

Fading deflation risks. While talk of deflation was all the rage early in the year this faded as commodity prices bottomed, spare capacity was gradually being used up and as the policy focus shifted from monetary to fiscal stimulus.

-

Rising commodity prices. An upswing in industrial commodity prices surprised many and was driven by a combination of better than feared demand and supply cuts.

-

Politics turned populist. The Brexit vote, the US election, the Australian election and some say the Italian referendum highlighted to varying degrees the rising support for populist solutions and a backlash against globalisation.

-

Another year of easy money. While growth fears and politics saw the Fed scale back its planned rate hikes, central banks in Europe & Japan remained in easing mode as did the People’s Bank of China during much of the year.

-

The great policy rotation. While monetary conditions remained ultra easy the realisation that monetary policy could only do so much combined with populist political pressures saw more talk of a shift towards fiscal stimulus. President elect Trump is at the pointy end of this move.

-

Low inflation saw more rate cuts in Australia and growth disappointed. Australian growth started off strong but weakened in the second half. Rebalancing is continuing, with NSW and Victoria continuing to do well, but a dip in inflation well below target saw the RBA continue cutting interest rates. Meanwhile, the risks continued to build around the Sydney and Melbourne housing markets.

While the macro environment turned out okay – the growth scare early in the year along with political events made for a constrained and at times interesting ride in investment markets.

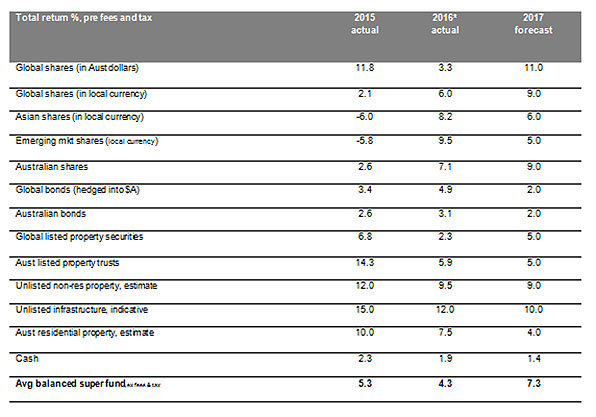

Investment returns for major asset classes

* Yr to date to Nov. Source: Thomson Reuters, Morningstar, REIA, AMP Capital

-

In contrast to 2015 that saw share markets start well and end badly, share markets started 2016 badly on growth and deflation fears before rebounding as such fears faded. The Brexit vote, the US election and the Italian referendum caused only short lived scares.

-

2016 saw a classic reversal of some of the relative share market performances that had been seen into 2015, with: US shares outperforming in developed markets as the Fed paused, the US earnings recession ended and investors anticipated stimulus under a Trump presidency; resources shares outperforming as commodity prices rebounded helping the Australian share market to perform relatively well; and emerging markets doing well led by Brazil.

-

After a huge rally in the first half of the year bonds then gave up their gains spurred along by anticipation of fiscal stimulus under Donald Trump. So bond returns were subdued.

-

Real estate investment trusts surged in the first half of the year, but fell as bond yields rose, constraining their returns

-

Unlisted commercial property and infrastructure continued to benefit as investors sought decent income yields.

-

Australian residential property returns were solid but slowed and remained concentrated in Sydney and Melbourne.

-

Cash rates and bank term deposit returns were poor reflecting record low RBA interest rates.

-

After several years of falls, the $A fell actually rose 3% as the Fed delayed and commodity prices rose.

-

Balanced superannuation funds returns were subdued, but better than cash and bank deposits.

2017 – looking better despite the noise

Of course those who foresaw the “financial crisis of 2016” will just roll their call into 2017! But there are good reasons to believe disaster will yet again be averted.

-

Leading growth indicators such as business conditions PMIs have reaccelerated after a 2015-16 soft patch and actually point to stronger growth.

Source: Bloomberg, IMF, AMP Capital

-

There is no sign of the sort of excesses that drive recessions & deep slumps in shares: there has been no major global bubble in real estate or business investment; inflation remains low; share markets are not unambiguously overvalued and global monetary conditions are easy.

-

While the Fed is likely to raise interest rates several times in 2017 this will likely be offset by fiscal stimulus from the Trump administration equal to around 1% of GDP. Rate hikes are likely to be limited to the extent that the rising $US is doing part of the Fed’s job.

-

Meanwhile monetary conditions will generally remain easy in the Eurozone and Japan with a further easing likely in Australia, albeit a tightening phase is possible in China.

Against this background:

-

Global growth is likely to move just above 3%, ranging from around 2% in advanced countries to around 6% in China.

-

Headline inflation is likely to continue to rise as commodity prices rise with core inflation rising more slowly.

-

The earnings recession looks to have ended – at least in the US & Australia – with solid earnings growth likely.

-

Bond yields have gone up too far too fast in the short term, but the trend is likely to be gradually up.

For Australia, the economy is likely to continue to rebalance away from mining investment and pick up again from its September quarter decline: the ramp up in resource export volumes has further to go; there is still a huge pipeline of housing activity yet to be completed; strengthening approvals point to stronger non-dwelling construction; the drag from mining investment is fading as it falls as a share of GDP and its likely to be close to a bottom next year; recent retail sales data have improved suggesting a consumer bounce back in the December quarter and the rebound in commodity prices tells us that the income recession in Australia is over. Expect Australian growth to be around 2.5% through 2017.

However, near term risks to Australian growth are on the downside, inflation is likely to remain below target for longer than the RBA is forecasting, the RBA is likely to need to offset increases in bank mortgage rates and the $A remains too high. So we expect another rate cut in the first half of next year taking the cash rate to 1.25%. A rate hike is a long way off.

Implications for investors?

The combination of some acceleration in global growth, rising profits and still easy money at a time when investors are highly sceptical (and ever fearful of the next GFC) should be positive for growth assets in 2017:

-

Global shares are likely to trend higher and we favour Europe (which is very cheap and likely to climb a wall of Eurozone break-up worries) and Japan (which will benefit from the lower Yen) over the US (which may be constrained after its 2016 outperformance and Fed rate hikes).

-

Emerging markets may underperform if the $US continues to rise on Fed hikes but for now are looking attractive if as we expect the rise in the $US takes a break early in 2017.

-

Australian shares are likely to have solid returns as resource sector profits surge following the rebound in bulk commodity prices, overall profits rise 10% and interest rates remain low. Expect the ASX 200 to reach 5800 by end 2017. In terms of sectors favour resources, retailers, and banks.

-

Commodity prices are at risk of a short term pause/pull back but should remain well up from their 2015-16 lows.

-

Still low yields and capital losses from a gradual rise in bond yields are likely to see low returns from bonds.

-

Commercial property and infrastructure are likely to continue benefitting from the ongoing search by investors for yield.

-

National capital city residential property price gains are expected to slow to around 3-4%, as the heat comes out of the Sydney and Melbourne markets and rising supply hits.

-

Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

-

The downtrend in the $A is likely to continue as the interest rate differential in favour of Australia narrows and it undertakes its usual undershoot of fair value. Expect a fall below $US0.70 but little change versus the Yen and Euro.

What to watch?

The main things to keep an eye on in 2017 are:

-

US economic policy under President Trump – in particular whether the focus is on fiscal stimulus and deregulation as opposed to starting a trade war with China;

-

How aggressively the Fed raises rates – faster inflation could speed it up putting more upwards pressure on the $US;

-

A rapid rise in bond yields – this would be bad for shares and growth assets but a gradual rise would be okay;

-

Elections in the Netherlands, France, Germany and maybe Italy which could reignite Eurozone break-up fears if anti-Euro populists win (which I doubt they will);

-

Whether China continues to avoid a hard landing;

-

Whether non-mining investment picks up in Australia – a failure to do so could see aggressive RBA easing – and how a surge in apartment supply impacts property prices; and

-

Ongoing geopolitical flare ups, eg in the South China Sea.

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He also provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.